Unicorn Initiative: Exits

In a recently released report, UC Hastings and Brattle researchers analyzed unicorn exits to better understand how many of them have successful outcomes.

The Unicorn Initiative: Exits

Prepared by

There is no shortage of unicorn lists, but these tallies leave key questions unanswered for policymakers:

What are the outcomes? How and when are unicorns exiting?

Until recently, systematic analysis of these questions was premature. Now, however, a critical mass of companies have been unicorns long enough to identify some patterns that may help policymakers and others understand better this relatively new and evolving market.

The joint report dives into the data, unearthing some unexpected outcomes – including many success stories and valuations that might surprise outsiders.

Newly-minted US unicorns surged during 2021, with 334 companies reaching unicorn status – meaning they had a post-money valuation of $1 billion or more. This is a 259% increase from 2020’s number of unicorns at 93. The trend in companies reaching unicorn status has been increasing each year since 2016.

Key Findings #1

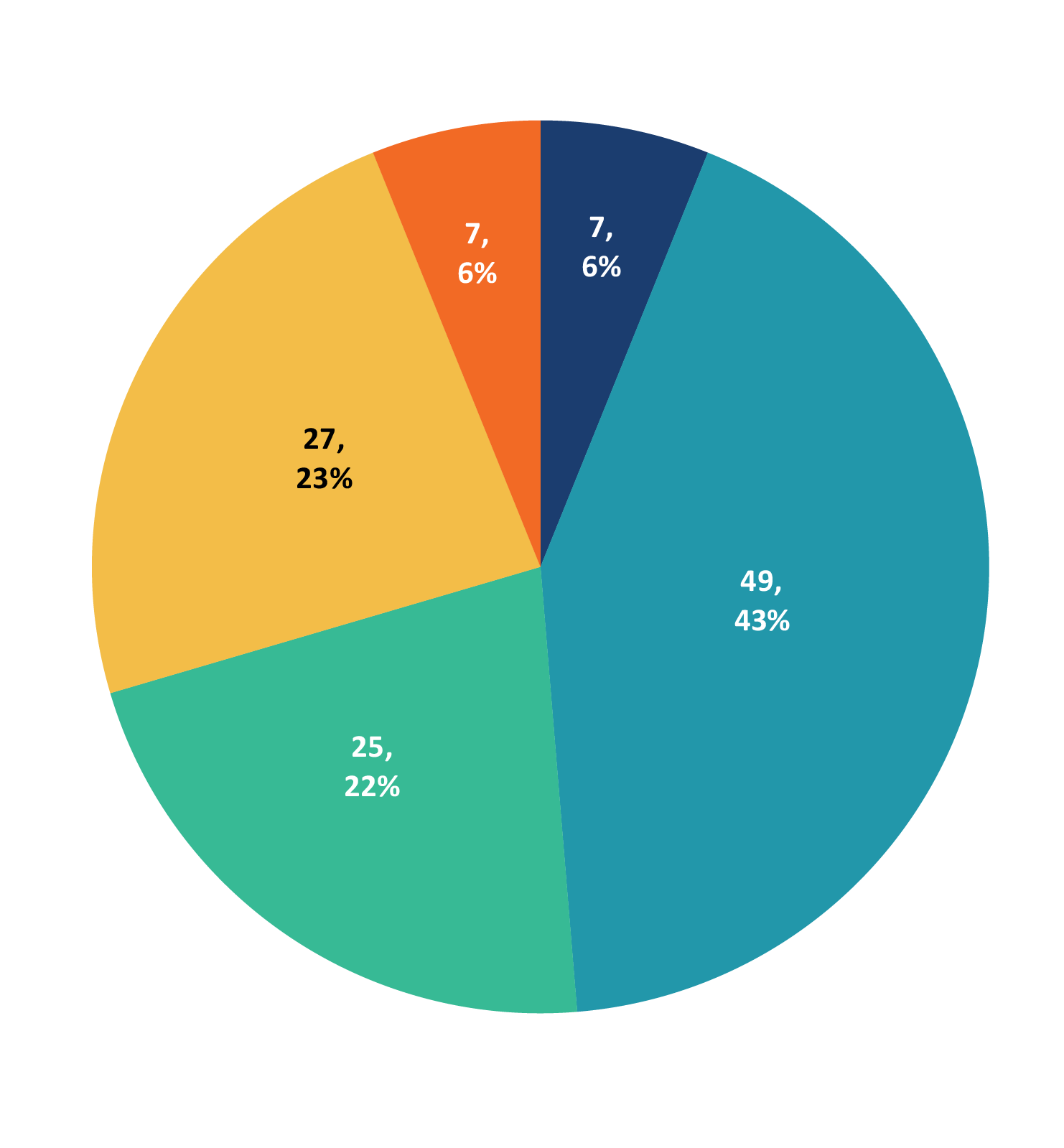

Overall, our findings indicate that the most common exit for unicorns is an IPO rather than mergers or acquisitions. Further, there is an emerging trend of reverse mergers as an exit outcome – i.e., SPACS – that is present in the full set of companies. Our findings somewhat contradict a prominent theme in corporate law and policy discussions – the death of the IPO. In fact, among the mature unicorns, an IPO is the most common outcome (49%, IPO plus reverse merger). This finding also sets unicorn startups apart from the general population of venture-backed startups, in which acquisitions remain the most likely outcome. According to a recent National Venture Capital Association report, there were over 8x more acquisitions than IPOs among all venture-backed companies in 2020.

Key Findings #2

Exit Status (All Cohorts)

Exit Status (Mature Cohorts)

Reverse Merger

IPO

Privately Held

Merger/ Acquisition

Out of Business/Bankruptcy

Mature unicorns that achieve public company status (IPO or reverse merger) and mature unicorns that exit by merger/acquisition are similar in terms of the two samples average post-money valuation, company age from first unicorn financing to exit, and average age at exit. However, the two categories of exits differ with respect to the average post-money valuation at exit and the total amount raised at exit. That is, for mature unicorns that go public, their post-money valuation at exit is more than twice as high as the mature unicorns that exit by merger/acquisition. Also, by the time of exit, companies that achieve public status have raised considerably more private financing ($2.2 billion) than companies that exit by merger/acquisition ($401 million).

Key Findings #3

SUMMARY STATISTICS FOR IPO/REVERSE MERGER VS. MERGER/ACQUISITION

Statistics

IPO/reverse merger (n=56)

merger/ acquisition (n=27)

Average “post-$ valuation” reported for the first unicorn financing

$1,675

$1,338

Average number of years from first unicorn financing to exit

3.2

3.2

Average “total amount raised” at exit deal*

$2,190

$401

Average “post-$ valuation” reported for the exit deal

$7,691

$3,382

Average age to exit

*Does not include exit deal value in amount raised

8.9

10.9

One way to measure the success of an exit is the ratio of the total capital raised to exit value (the “exit multiple”). By this metric, IPOs are not always outsized successes. A majority of the IPOs/reverse mergers achieve exit multiples of less than five. This analysis also shows that, while some mergers may be fire sales that return less than total capital invested, other mergers achieve comparatively high exit multiples of over 20. In short, IPO/reverse mergers are not always clear successes and merger/acquisitions are not all disappointments.

Key Findings #4

SUMMARY STATISTICS FOR IPO/REVERSE MERGER VS. MERGER/ACQUISITION

Post-$ Valuation/Total Raised…

<1

<5

<10

>10

>20

Exit Type

Merger/ acquisition

8

7

5

3

3

IPO/ reverse merger

4

37

11

4

0

Finding #1

Finding #2

Finding #3

Finding #4

Key Questions

authors

about brattle

The Brattle Group answers complex economic, finance, and regulatory questions for corporations, law firms, and governments around the world. We are distinguished by the clarity of our insights and the credibility of our experts, which include leading international academics and industry specialists. Brattle has 500 talented professionals across North America, Europe, and Asia-Pacific.

The Center for Business Law at UC Hastings was founded with the mission of bringing together leading scholars, business leaders, practitioners, regulators, and students to engage in the study, teaching, and practice of business law at UC Hastings. The Center aims to be the leading business law venue in San Francisco, one of the world’s great centers of commerce, finance, and technology.

about UC Hastings Center for Business Law

How do we define unicorn companies?

Why is it important to research unicorn outcomes?

Are the reports of the death of the IPO greatly exaggerated?

Abe Cable

Professor of Law

UC Hastings

Adrienna Huffman

Associate

The Brattle Group

Monet Lee

Research Analyst

The Brattle Group

Shuyi Deng

Jr. Business Analyst

Former Brattler